MQ, FLYW Previews

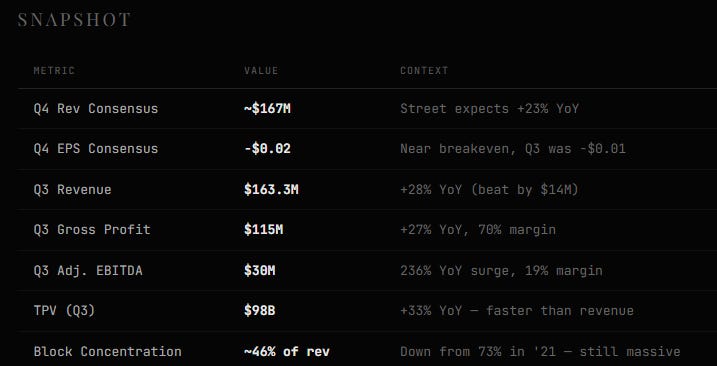

Marqeta (MQ)

Marqeta has been my favorite short pick for a while now, essentially since IPO. Stock was tied heavily to huge amounts of stimulus and the neobank boom, and sell-side analysts got incredibly lazy on the name. Every analyst picked a buy or a positive hold to get corp access, while everyone overlooked the stretched valuation, customer concentration, and problems within the tech stack. Here’s what I’m paying attention to.

Cash App Transition: Cash App Card’s new issuance is transitioning to Bancorp, meaning new Cash App cards are no longer processed through Marqeta. Existing cards remain on Marqeta’s rails, but the growth engine of Cash App is migrating away. Any quantification of the revenue impact timeline or acceleration of the transition would kill the name.

Gross profit decel: MQ guided Q4 gross profit growth of 17–19% YoY, a sharp deceleration from 27% in Q3. Revenue guidance of 22–24% also steps down from 28%. The gap between TPV growth (33%) and revenue growth (28%) and gross profit growth (27%) shows unfavorable mix toward lower-margin processing-only programs. If Q4 gross profit comes in at the low end (~$112M) or below, it confirms the take-rate compression thesis.

FY26 Guide: If management guides below mid-teens GP growth or signals accelerating Cash App attrition, the stock has no floor. MQ is a ~$2B market cap name that likely won’t ever become GAAP profitable, in a space becoming increasingly commoditized and a sub-par tech stack. Not the most ideal place for investors to look for a long in this tape.

Where we could be wrong: Europe is growing >100% YoY and MQ closed the €46M TransactPay acquisition in July ‘25 to provide BIN sponsorship across UK/EEA. If Europe revenue is quantified and material ($20M+ run rate), it offsets some Cash App anxiety. But Europe remains <10% of total revenue — it’s too small to save the story.

Lending and BNPL use cases grew >60% in Q3, accelerating 10 points sequentially. Visa Flexible Credential adoption is driving broad-based volume. This is the strongest non-Cash App growth vector and the core of the bull case for diversification. If BNPL/lending TPV continues to accelerate and management quantifies it as a percentage of total, it could shift the narrative. I do want to note that KLAR had a particularly bad quarter, so it will be interesting to see that impact on MQ.

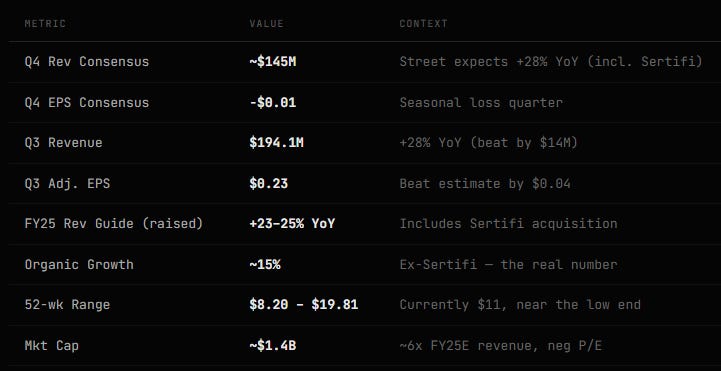

FlyWire (FLYW)

International student enrollment: Management flagged ‘mid-single-digit growth headwinds in 2026’ on the Q3 call, specifically citing lower student visa issuances. Flywire’s education vertical is ~55% of revenue and heavily indexed to cross-border tuition payments. The Trump administration’s immigration restrictions, combined with UK/Australia/Canada tightening visa policies, are creating a structural headwind. If Q4 education payment volume shows any deceleration or FY26 guide reflects >5% organic headwinds, the stock has further to fall.

Sertifi: Sertifi contributed $12.9M in Q3 revenue and added 8 percentage points to YoY growth. Without it, organic revenue growth was ~20% in Q3, lower than the headline 28%. For FY26, the Sertifi comp normalizes in H2, meaning headline growth could drop to mid-teens organic by Q3/Q4 ‘26. If management guides FY26 revenue growth at 15% or below organically, there will be a multiple re-rating to the downside.

FY26 Guide: Management pre-warned of mid-single-digit growth headwinds in 2026. The question is how conservative they embed this into the FY26 guide. Consensus expects ~$700–720M FY26 revenue, implying ~15% growth. The bar is higher in this tape - in-line or worse and the stock gets punished.

Where we could be wrong: If healthcare and travel can grow fast enough to offset education headwinds, the ‘diversified payments platform’ narrative survives. Watch for segment-level disclosure or color on non-education growth rates. Bulls argue that moving 20–25 universities onto SFS could add >$50M in revenue, a significant organic growth lever independent of cross-border student flows. The DACH region integration with academyFIVE (Feb ‘26) extends this thesis. But SFS is a longer sales cycle and the near-term revenue impact is uncertain. This is a 2027+ story, not a Q4 catalyst.